Funding Investments In Early Care And Education

Since the Inflation Reduction Act did not contain any additional funding for early childhood care and education, the two ideas with current Republican support are reforming the child tax credit and the child care development block grant. In looking to fund these worthwhile initiatives, Congress should look to funding sources that primarily affect high-income families: the estate tax and the mortgage interest deduction.

Senators Mitt Romney, Richard Burr (NC) and Steve Daines (Mont) have proposed the Family Security Act 2.0 to expand the Child Tax Credit for working families. So far, it is just a summary proposal without bill text. The child benefit provisions improve the current child tax credit, with the notable exception of excluding U.S. citizen children living in mixed-status families. The proposed means to pay for this credit, however, particularly the revisions to the Earned Income Tax Credit and eliminating Head of Household filing status, improperly places the burden to pay for the increased CTC on low- and moderate-income families.

Senator Tim Scott and eleven other Republican Senator co-signers have introduced the CCDBG Reauthorization Act 2022. This increases family eligibility from 85% of state median income up to 150% SMI and introduces a sliding scale for family co-pays so that families earning less than 75% of SMI would not pay anything out of pocket:

These changes are welcome, but become meaningless unless additional funding is provided. Under current funding, without the expansion proposed by Senator Scott, only 9.5% of eligible children in Utah under age 6 are served by CCDBG funds. In order to fund early childhood investments, Congress should analyze the tax benefits provided to second homeowners and the estate tax.

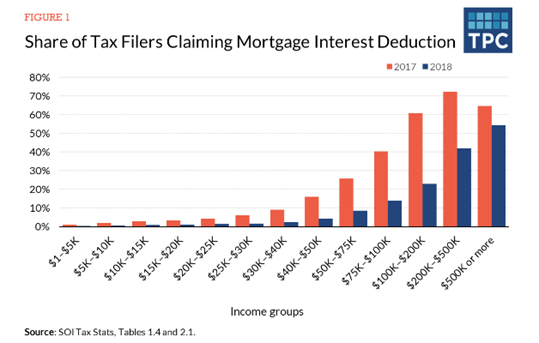

Congress should eliminate the mortgage interest deduction on the estimated 7.5 million second homes in the U.S. According to the Tax Policy Center, reducing the mortgage interest deduction as part of the Tax Cuts and Jobs Act (TCJA) did not hurt home values as feared by critics, and the majority of households who claim this deduction are high-income.

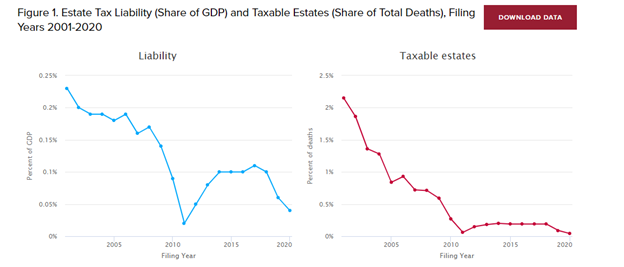

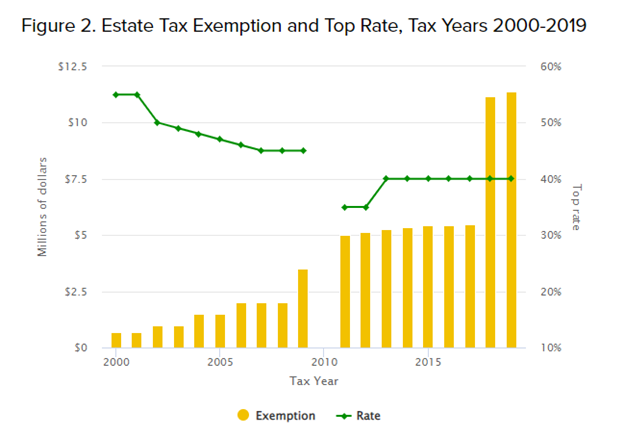

Another potential funding source is to reduce the estate tax exemption. Currently, each estate may claim an exemption at $12.06 million per person, which is more than double the amount ($5.49 million) permitted prior to 2018 when the TCJA law increased it. The Penn Wharton Budget Model predicts that the federal estate tax would have generated 9 times more revenue in 2019 without the tax changes in 2001 and 2017. According to the Tax Policy Center, in 2017 the total amount of net estate tax paid was $19,940,000,000. In 2020, the total amount of net estate tax paid was $9,334,000,000, reduced by over half. Notably, Californians paid the most at $2,325,634,000 while Utahns could not be shown in the chart for fear of disclosing individual taxpayer data. Raising the exemption threshold in the TCJA lost $10,606,000,000 in 2020 as compared to 2017.